Gage Bowser

Affiché le Dec 29,2023

AscendEX Sunday Briefing (12.24-12.31)

Something to remember:

“Through discipline, though not through discipline alone, we can achieve serenity, and a certain small but precious measure of freedom from the accidents of incarnation . . . and through discipline we learn to preserve what is essential to our happiness in more and more adverse circumstances, and to abandon with simplicity what would else have seemed to us indispensable."

The Week Ahead

What’s driving markets?

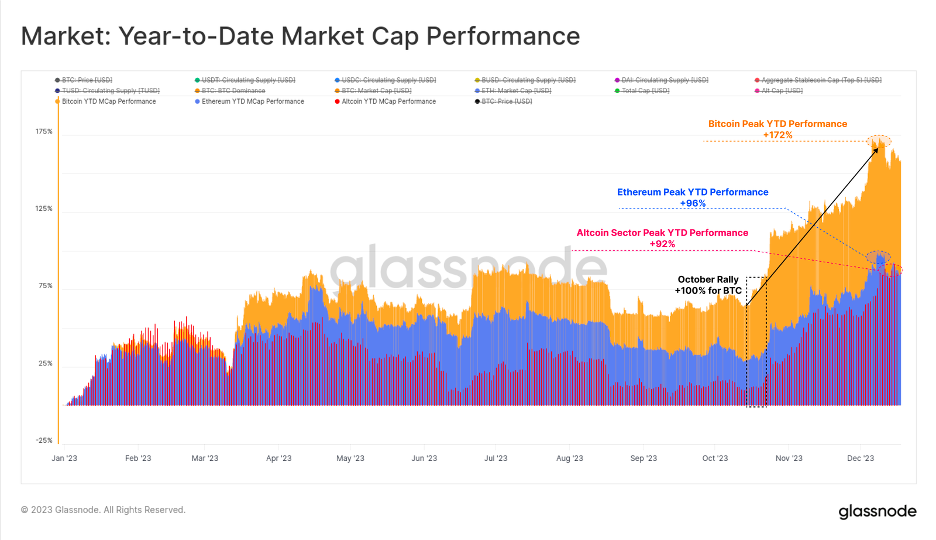

Bitcoin is up 172% on the year, storming out of the volatility drought of H1 2024 amidst what seems to be a perfect storm of bullish catalysts. Bitcoin spot ETFs

Bitcoin and Ethereum are trading ~40%, ~50% from all time highs, respectively.

The crypto market is quite euphoric. The Fear and Greed index is flashing a 71 (greed), and on a 5 year timeframe, most investors are now in profit.

Catalysts

Thursday, December 28th @ 8:30AM ET: US Initial Jobless Claims.

Year of the Dragon Bull

I present to you my 2024 crypto market predictions:

Centralized Exchanges continue to bleed volume market share to DEXes. As the average crypto trader becomes more comfortable with trading on-chain, while the user experience of mobile wallets and decentralized applications continues to improve, CEXes will see their market share of volume for both spot and derivatives trading continue to dwindle. As we have already begun to see, major CEX have sought to combat this trend through various methods, pushing a “Hybrid CEX” model to varying degrees. OKX has built an entire web3 suite, allowing users to interact with decentralized applications via their own interface. Coinbase has launched an Ethereum Layer 2 (BASE). Wallets and aggregators are pursuing partnerships with Centralized Exchanges to gain access to their users’ flows as they begin setting off from the custody of a CEX to go on-chain. In the limit, however, decentralized exchanges are still unable to offer a trading experience that fully matches the high throughput and low latency of off-chain matching via a central order book. What’s more, the ability to cycle fresh addresses using a CEX’s omnibus wallet system is still an attractive use-case for the Centralized Exchange, as similar decentralized applications like Tornado Cash have been sanctioned.

Crypto returns increasingly form a barbell distribution. A major trend of 2023 which I suspect will continue has been the proliferation of low-effort, rapid-launch meme tokens. Projects like HPOS10I, Pepe, and various dog-themed coins captured the mid-summer zeitgeist as traders bored with the lack of volatility sought returns wherever they could be found. Galvanized by new tools that streamline creation, tracking and trading of this cohort of tokens, the memecoin sector saw by far the biggest growth this year. This has resulted in a liquidity vacuum from mid-tier assets that traditionally would have caught a bid, creating a barbell-like distribution in returns in crypto as traders focus on a portfolio consisting of“blue-chips”, such as BTC and ETH, and risky bets like memecoins.

Bitcoin dominance begins to trend downward again. Bitcoin dominance has grown ~10% in 2023 to roughly 50%. This is a standard occurrence for the beginning of a bullish period in crypto, where Bitcoin leads the market forward followed by periods of price consolidation where traders diversify into market beta seeking higher returns. This cycle, the front-loading effect of Bitcoin dominance has been amplified by ETF approval expectations. However, with on-chain activity at all-time-highs, more robust DeFi, and more mature gaming/socialfi verticals, traders have more reason than in previous cycles to diversify their crypto holdings into more than just Bitcoin.

Fundraising will focus more on Consumer Applications. Last cycle saw crypto VCs pour billions of dollars into alternative protocols and execution layers such as Aptos, Sui, various Zk-EVMs and L2s, modular data availability solutions, and other infrastructure. Now as many of these products have since gone live, the elephant in the room has become impossible to ignore. Despite all of the innovation solving for the supply side of the blockchain equation (increasing throughput, decreasing fees), there now appears to be a lack of demand. The question for crypto venture capitalists is, who is going to use all of this blockspace? This cycle should see the lion’s share of funding go towards consumer applications built leveraging improved infrastructure. Socialfi application FriendTech was an early indication of this trend, securing Paradigm as a lead investor this past August.

Volatility not to reclaim 2021 peak. Crypto has matured significantly, and we are now on the brink of the industry’s first spot ETF approval. While this does open the floodgates for institutional capital, increased legitimacy, and millions of dollars of new liquidity, those who treasure crypto for its outsized volatility will be disappointed. The Chicago Mercantile Exchange (CME) has surpassed any crypto-native venue in open interest, actually dwarfing Binance’s bitcoin OI by 4x. The rise in prominence of liquid options venues and other sophisticated instruments will foster a more orderly marketplace for crypto’s major assets. As the majority of the market remains highly correlated and trades in some degree as blue chip beta, it stands to reason that it is unlikely market

Charts

Bitcoin will close out 2023 as the second best performing risk-adjusted financial asset

The majority of the crypto market’s gains this year came in Q4 as the Fed completed its hiking cycle and ETF optimism gripped the market

Sol/ETH ratio has traded to its highest level since before the FTX implosion

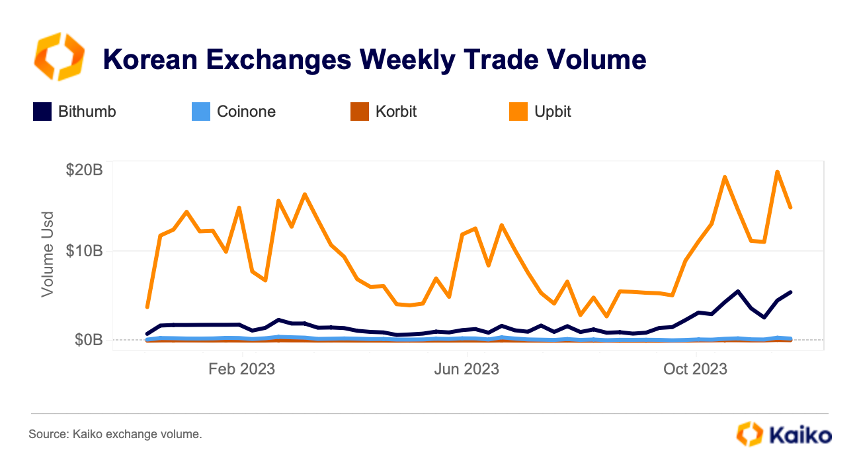

Korean exchanges, whose volume is highly concentrated in altcoins relative to other exchanges, have seen volumes surge to yearly highs in the past month

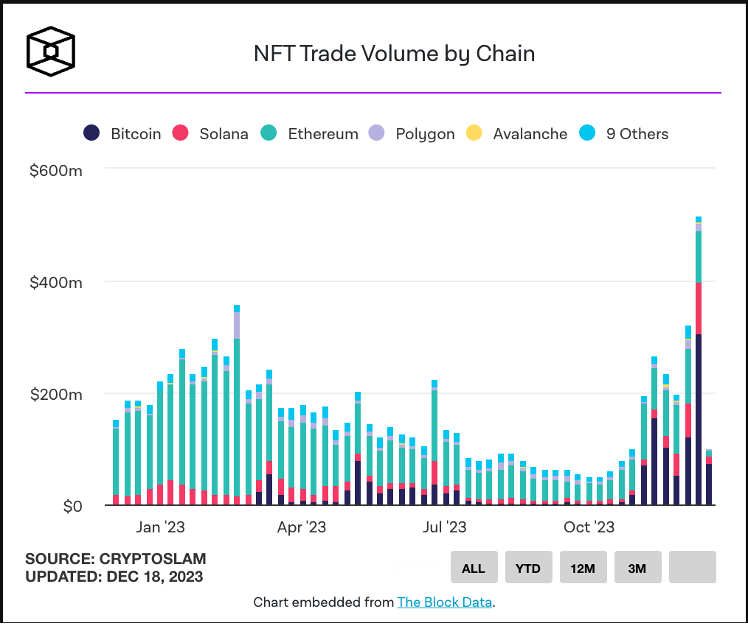

NFT trading volume on the Bitcoin network has surpassed all other chains in the past quarter, and OKX’s Ordinals exchange has surpassed Blur and Opensea to take the top NFT trading exchange by volume. Neither Blur nor Opensea have integrated Ordinals trading

Research Content

Inscriptions dashboard

Kaiko crypto year in charts

BVI court freezes $1B in 3AC assets

A16z’s 2024 crypto predictions

Solana volume flips ETH on most major exchanges

Bitwise ETF commercial

Coinbase invites Elizabeth Warren to a briefing

Arthur Hayes blogs about Bitcoin ETFs

Crypto firms are ramping up political donations

Glassnode’s 2023 on-chain report

Binance CFTC settlement approved by a judge

Disclaimer: AscendEX and its affiliates do not provide financial, legal, tax or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, financial, legal, tax or accounting advice. This does not constitute an offer to issue or sell, or a solicitation of an offer to subscribe, buy, or acquire an interest in, any securities, financial instruments or other services, nor does it constitute a financial promotion, investment advice or an

This material is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation, or which would subject AscendEX to any registration requirement within such jurisdiction or country. Information